Over seventy percent of American ecommerce businesses report delays and extra costs when accepting payments from Canada, the United Kingdom, and other international markets. When a single payment hiccup can stall a cross-border sale, finding the right international payment method matters more than ever. This guide breaks down each reliable option, helping ecommerce managers cut through complexity and choose methods that make overseas sales simpler and safer.

Table of Contents

- What International Payment Methods Involve

- Key Types for U.S. Ecommerce Merchants

- How Payment Gateways and Providers Work

- Cost, Settlement, and Compliance Factors

- Managing Risks and Avoiding Common Pitfalls

Key Takeaways

| Point | Details |

|---|---|

| Understanding Payment Methods | Various international payment methods like EFT, wire transfers, and cryptocurrencies have distinct advantages and challenges, impacting businesses’ choice for cross-border transactions. |

| Importance of Compliance | Merchants must navigate regulatory environments, focusing on compliance to avoid penalties and ensure secure transactions. |

| Risk Management | Implementing robust fraud detection and adaptive security measures is essential to mitigate risks associated with international payments. |

| Cost-Benefit Analysis | Conduct regular evaluations of transaction fees and performance of payment methods to ensure they align with business goals and customer preferences. |

What International Payment Methods Involve

International payment methods represent sophisticated financial mechanisms designed to facilitate secure monetary transactions across different countries and currencies. These methods go beyond traditional bank transfers, incorporating advanced technologies and digital platforms that enable seamless cross-border commerce. Global payment technologies have evolved dramatically, transforming how businesses exchange funds internationally.

Most international payment methods can be categorized into several key types:

- Electronic Funds Transfer (EFT): Direct digital transfer of money between bank accounts

- Wire Transfers: Bank-to-bank transactions using networks like SWIFT

- Credit/Debit Card Payments: International card processing networks

- Digital Wallets: Online payment platforms supporting multiple currencies

- Cryptocurrency: Blockchain-based digital currency transactions

- Foreign Currency Accounts: Specialized bank accounts for international transactions

Digital payment infrastructure now supports multiple transaction types, allowing businesses unprecedented flexibility in how they manage international financial exchanges. Modern payment systems integrate real-time currency conversion, fraud protection, and compliance tracking to streamline cross-border transactions.

Here is a comparison of key international payment methods and their core business impacts:

| Payment Method | Settlement Speed | Typical Use Case | Key Compliance Challenge |

|---|---|---|---|

| Electronic Funds Transfer | 1-2 business days | Routine business payments | Bank documentation requirements |

| Digital Wallets | Instant to 1 day | Online retail purchases | Customer verification standards |

| Cryptocurrency | Minutes to 1 hour | High-speed, low-fee transfers | Regulatory uncertainty |

| Foreign Currency Accounts | 1-3 business days | Multi-currency management | Ongoing KYC/AML reviews |

The core objective of international payment methods is reducing friction in global commerce. These systems must navigate complex challenges like currency exchange rates, transaction fees, regulatory compliance, and security protocols. Small to mid-sized retailers require payment solutions that balance cost-effectiveness with robust security features, enabling them to expand their market reach without compromising financial integrity.

Pro tip: Before selecting an international payment method, always conduct a comprehensive cost-benefit analysis comparing transaction fees, conversion rates, and platform reliability to ensure optimal financial performance.

Key Types for U.S. Ecommerce Merchants

U.S. ecommerce merchants have several strategic payment method options for facilitating international transactions. Payment technologies in e-commerce have evolved significantly, offering robust solutions tailored to cross-border sales requirements. Understanding these methods is crucial for expanding global market reach and ensuring smooth financial operations.

The primary payment methods for U.S. merchants include:

- Credit Card Payments: Widely accepted globally with strong security protocols

- Digital Wallets: Instant, low-fee international transaction platforms

- PayPal: Trusted intermediary with extensive international coverage

- Bank Transfers: Direct account-to-account transactions

- Buy Now, Pay Later (BNPL): Emerging financing option for international purchases

Digital payment landscapes demonstrate that consumer preferences are increasingly shifting toward convenient, secure online payment solutions. Each method offers unique advantages in terms of transaction speed, fees, currency conversion capabilities, and regulatory compliance.

Selection of the right payment method requires careful evaluation of factors like transaction volumes, target international markets, customer demographics, and risk management strategies. Small to mid-sized retailers must balance transaction costs, conversion rates, security features, and platform reliability to optimize their international sales potential.

Pro tip: Implement a multi-payment strategy that offers customers at least three different international payment options to maximize conversion rates and accommodate diverse consumer preferences.

How Payment Gateways and Providers Work

Payment gateways function as critical technological intermediaries that enable secure financial transactions between merchants, customers, and financial institutions. Payment gateway infrastructure represents a complex network of digital systems designed to validate, authorize, and process online payments with precision and security.

The typical payment gateway workflow involves several key stages:

- Authorization Request: Customer initiates payment

- Encryption: Sensitive financial data gets securely encoded

- Bank Communication: Transaction details transmitted to acquiring bank

- Verification: Bank checks customer account and transaction validity

- Approval/Rejection: Transaction status determined

- Confirmation: Result communicated back to merchant and customer

Digital payment infrastructures have evolved to support increasingly complex cross-border transactions, integrating advanced security protocols and real-time verification mechanisms. These systems must navigate multiple regulatory environments, currency conversions, and technological standards while maintaining rapid transaction processing speeds.

For small to mid-sized U.S. ecommerce merchants, selecting the right payment gateway involves evaluating factors like transaction fees, international currency support, fraud prevention capabilities, integration complexity, and customer experience. Successful implementation requires understanding how these technological platforms can streamline financial operations and reduce potential risks associated with global online sales.

Pro tip: Always conduct thorough technical compatibility testing with potential payment gateways and maintain multiple payment method options to ensure seamless transaction experiences for international customers.

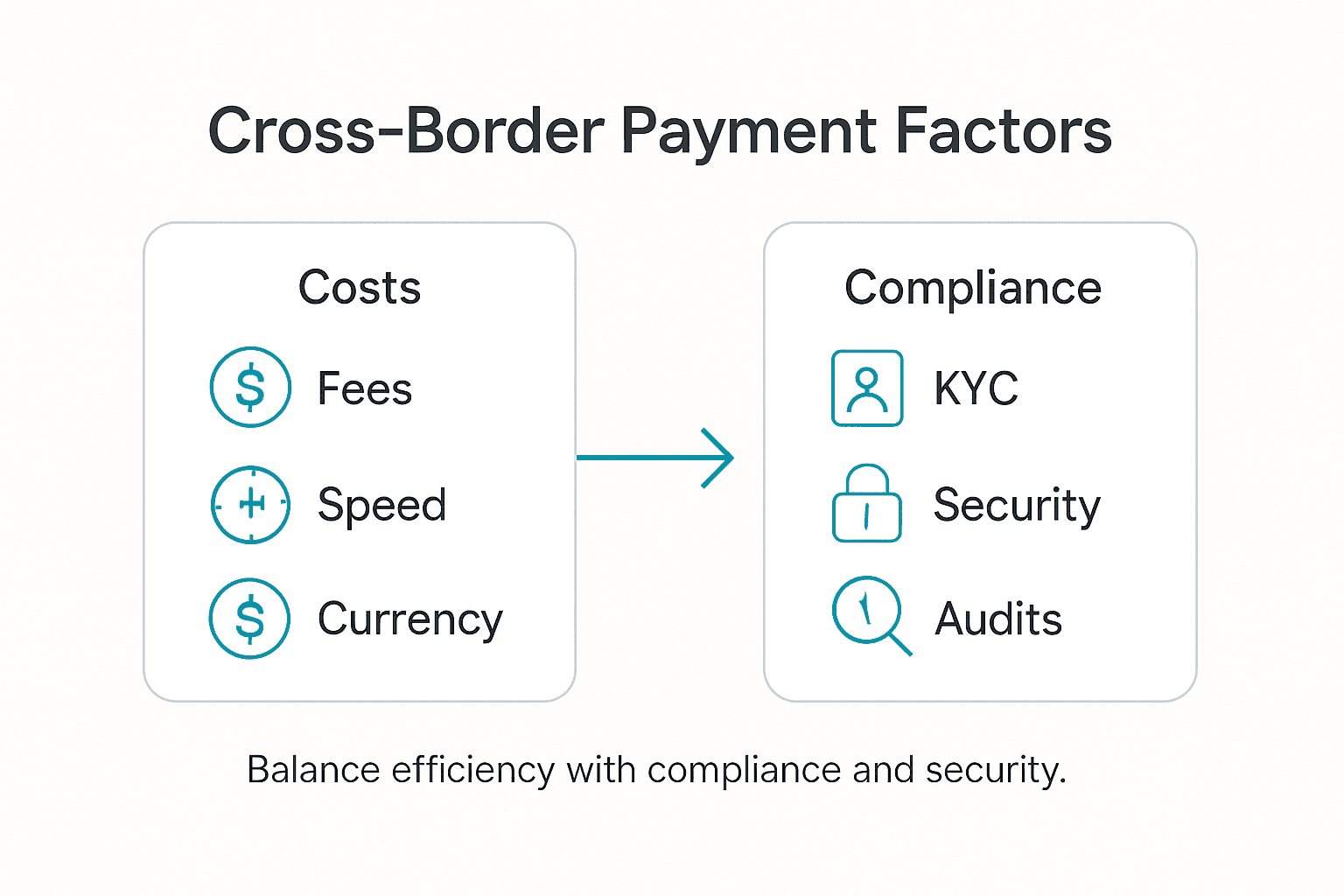

Cost, Settlement, and Compliance Factors

International payment transactions involve complex financial considerations that extend far beyond simple money transfer mechanics. Cross-border payment cost determinants encompass multiple interconnected factors including currency exchange rates, transaction fees, regulatory compliance expenses, and technological infrastructure investments.

Key cost and compliance elements for U.S. merchants include:

- Transaction Fees: Percentage-based charges for international payments

- Currency Conversion Rates: Fluctuating exchange rate margins

- Regulatory Compliance Costs: Anti-money laundering (AML) and Know Your Customer (KYC) requirements

- Security Infrastructure Investments: Fraud prevention and data protection systems

- Settlement Timelines: Duration between transaction initiation and fund availability

- Geopolitical Risk Factors: Potential restrictions or sanctions impacting international transactions

Payment method compliance frameworks have become increasingly sophisticated, requiring merchants to navigate complex regulatory landscapes. Small to mid-sized U.S. ecommerce retailers must carefully evaluate these multifaceted expenses, understanding that lower upfront transaction costs might be offset by hidden compliance or currency conversion expenses.

Successful international payment strategies demand a holistic approach that balances cost efficiency with robust security protocols. This involves continuously monitoring transaction expenses, staying updated on regulatory changes, and implementing flexible payment systems that can adapt to evolving global financial requirements.

Pro tip: Conduct quarterly comprehensive audits of your international payment infrastructure to identify potential cost-saving opportunities and ensure ongoing regulatory compliance.

Managing Risks and Avoiding Common Pitfalls

International payment transactions present complex risk management challenges that require strategic planning and proactive monitoring. Cross-border payment risk frameworks highlight the critical importance of developing comprehensive strategies to mitigate potential financial vulnerabilities.

Common international payment risks include:

- Fraudulent Transaction Detection: Unauthorized payment attempts

- Currency Fluctuation Exposure: Unexpected exchange rate variations

- Compliance Violations: Regulatory infractions leading to potential penalties

- Chargeback Management: Disputed transaction resolution processes

- Data Security Breaches: Potential compromise of financial information

- Payment Gateway Reliability: Technical failures interrupting transaction flows

Merchant payment risk mitigation strategies emphasize the need for multi-layered security approaches. Small to mid-sized U.S. ecommerce retailers must implement robust verification protocols, real-time transaction monitoring, and adaptive fraud prevention systems that can quickly identify and neutralize potential threats.

Successful risk management requires continuous education, technological investment, and a proactive approach to identifying emerging financial security challenges. Merchants should develop flexible frameworks that can rapidly adapt to changing international payment landscapes, integrating advanced machine learning algorithms and comprehensive compliance tracking mechanisms.

Below is a summary of key risk management techniques for international payments:

| Risk Type | Mitigation Technique | Example Benefit |

|---|---|---|

| Fraud Detection | AI-powered transaction monitoring | Early identification of anomalies |

| Currency Fluctuation | Automated exchange rate hedging | Protects profit margins |

| Compliance Violations | Real-time regulation alerts | Reduces penalty and audit risk |

| Data Security Breaches | End-to-end encryption | Safeguards sensitive information |

Pro tip: Implement a quarterly comprehensive risk assessment process that includes external security audits, transaction pattern analysis, and continuous staff training on emerging fraud prevention techniques.

Streamline Your Cross-Border Sales with Reliable Courier Services and Logistics Solutions

Expanding international sales means overcoming challenges like payment complexities, regulatory compliance, and timely delivery. The article highlights how navigating international payment methods requires balancing speed, security, and cost while managing risks like fraud and currency fluctuations. To truly boost cross-border success, your ecommerce business needs more than just payment solutions — it requires an integrated logistics partner that ensures your products reach customers quickly and safely.

At or-ner.com, we offer comprehensive end-to-end logistics tailored to ecommerce sellers who demand reliability at every step. Our platform supports real-time shipment tracking, customs clearance, and efficient fulfillment across a global network of warehouses designed to reduce delays and avoid costly compliance pitfalls. Combining our advanced logistics with a strong payment strategy means smoother international operations and happier customers.

Elevate your global ecommerce game with:

- Flexible, scalable shipping options that align with your international payment workflows

- Improved visibility and control over every shipment

- Support for multiple transport modes ensuring fast, reliable delivery

Ready to eliminate cross-border headaches and seize new markets confidently?

Explore how our reliable courier services and supply chain expertise can complement your international payment methods now.

Get started today at or-ner.com and transform your cross-border sales with logistics you can trust. Learn more about our solutions for streamlined ecommerce growth at or-ner.com.

Frequently Asked Questions

What are the key international payment methods available for businesses?

International payment methods include Electronic Funds Transfers (EFT), wire transfers, credit and debit card payments, digital wallets, cryptocurrency transactions, and foreign currency accounts. Each method offers unique advantages depending on the business needs.

How do payment gateways facilitate international transactions?

Payment gateways act as intermediaries that securely process transactions between merchants and customers by validating and authorizing payments, ensuring sensitive data is encrypted and protected throughout the process.

What factors should businesses consider when selecting an international payment method?

Businesses should consider transaction fees, currency conversion rates, settlement speed, compliance requirements, and security features to determine the most cost-effective and efficient payment methods for their operations.

How can businesses manage risks associated with international payments?

To manage risks, businesses should implement multi-layered security approaches, such as AI-powered fraud detection systems, real-time regulation alerts for compliance, and robust verification protocols to safeguard against unauthorized transactions and data breaches.