TL;DR:

- Freight insurance protects businesses and ecommerce sellers against financial losses from damaged, lost, or stolen goods during transit.

- Understanding coverage types, exclusions, and claim procedures helps sellers recover losses more effectively.

- Operational habits like proper packaging and timely reporting are key to ensuring claims are paid.

Freight insurance is defined as specialized cargo coverage that protects businesses and ecommerce sellers against financial loss when goods are damaged, lost, or stolen during transit. The industry standard term is “cargo insurance,” though “freight insurance” is widely used interchangeably in ecommerce and logistics circles. Understanding freight insurance basics means knowing the difference between all-risk and named perils policies, recognizing what carriers actually owe you by law, and knowing how to file a claim that actually gets paid. Every seller shipping physical goods faces real exposure to loss, and the gap between what you think you’re covered for and what a policy actually pays is where most financial pain lives.

What are the main freight insurance basics every seller should know?

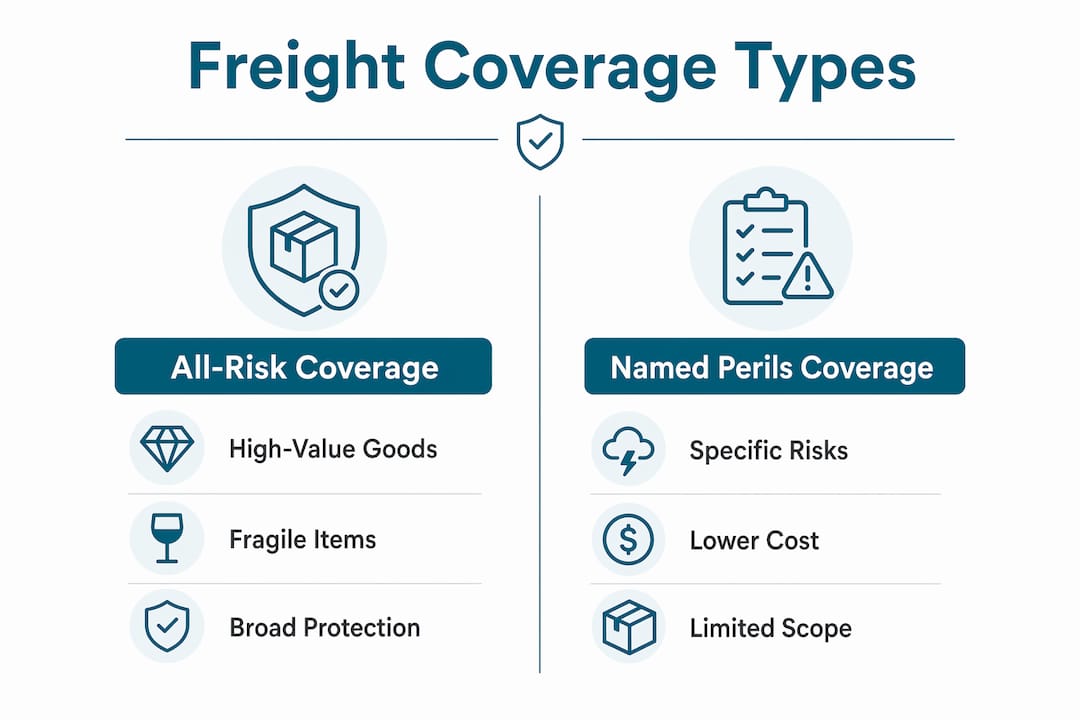

Freight insurance coverage falls into two broad categories: all-risk and named perils. All-risk coverage protects against nearly every cause of physical loss or damage during transit, except for a defined list of exclusions. Named perils coverage only pays for losses caused by specific events listed in the policy, such as fire, collision, or theft.

Two additional policy types matter for ecommerce sellers. Total loss only coverage pays out solely when an entire shipment is destroyed or lost, not for partial damage. Shipper’s interest coverage is purchased directly by the cargo owner and pays based on the commercial invoice value of the goods, not the carrier’s liability cap.

Contingent cargo insurance is a separate category used by freight brokers and third-party logistics providers. It activates when a carrier’s primary insurance fails to respond. Sellers working with 3PLs should confirm whether their provider carries this layer of protection.

Common policy endorsements add coverage for specific risks not included in a base policy. The most requested endorsements include temperature control (for perishables), theft from unattended vehicles, and strikes or civil unrest. Each endorsement adds cost but closes a gap that base policies leave open.

| Coverage Type | Typical Best Use | Key Limitation |

|---|---|---|

| All-risk | High-value or fragile goods | Excludes packaging failures and inherent vice |

| Named perils | Budget-conscious, lower-risk routes | Only pays for listed events |

| Total loss only | Bulk commodity shipments | No partial damage payout |

| Shipper’s interest | Direct cargo owners | Requires accurate invoice documentation |

| Contingent cargo | 3PLs and freight brokers | Secondary layer, not primary coverage |

Pro Tip: Read the exclusions list before the coverage list. What a policy does not cover tells you more about your real risk exposure than what it does cover.

What does freight insurance typically cover and exclude?

All-risk policies cover physical loss or damage from collision, fire, theft, flooding, and certain weather events during transit. That list sounds broad, but the exclusions are where most sellers get surprised.

The most common exclusions across freight insurance policies include:

- Inadequate packaging: If your goods arrive damaged and the insurer determines the packaging was insufficient, the claim is denied.

- Inherent vice: Natural deterioration or spoilage that occurs regardless of handling, such as fruit rotting or metal corroding.

- Delay: Freight insurance policies almost never cover financial losses caused by late delivery, even when the shipment value is high.

- War and strikes: Standard policies exclude losses from armed conflict, strikes, and civil unrest unless a specific endorsement is purchased.

- Unattended vehicle clauses: Many policies void theft claims if cargo was left in an unsecured or unattended vehicle overnight.

Claim denials rarely happen because a policy is poorly written. They happen because the shipper violated a condition buried in the fine print. Packaging failures and unattended vehicle clauses are the two most common triggers for denied freight insurance claims.

Conditional coverage requirements are real and enforceable. Some policies require that vehicles be parked in secured, monitored lots overnight. Others specify minimum packaging standards by commodity type. Sellers who skip these conditions do not just risk a denied claim. They risk absorbing the full cost of a loss that felt covered.

Pro Tip: Before shipping high-value goods, photograph your packaging process. Timestamped photos showing proper cushioning, box integrity, and labeling are your first line of defense if a claim is disputed.

How does the freight insurance claims process work?

Filing a freight insurance claim follows a defined sequence. Missing any step, or missing a deadline, can reduce or eliminate your payout. Incident reporting must happen within 30 days of the loss event, and supporting evidence must be submitted for assessment within 7–30 days after that.

The standard claims process runs in this order:

- Report the incident immediately. Notify your insurer as soon as you discover loss or damage. Do not wait for the carrier’s investigation to conclude.

- Document everything at delivery. Note exceptions on the delivery receipt before the driver leaves. A clean delivery receipt with damage discovered later is much harder to claim.

- Collect photographic evidence. Photos of damage, the original packaging, and the shipping label are required by virtually every insurer.

- Gather supporting documents. Assemble the commercial invoice, packing list, bill of lading, and any carrier correspondence.

- Submit the claim with all evidence. Incomplete submissions restart the clock and delay assessment.

- Follow up within the assessment window. Claims processing runs 7–30 days once all documents are received. Track your submission date.

The most common pitfall is assuming the carrier will handle the documentation. Carriers have their own interests in a claim. You need your own parallel record. Sellers who maintain a shipment log with photos, weights, and packaging details resolve claims faster and at higher rates than those who rely on memory or carrier records alone.

Pro Tip: Create a claims folder for every high-value shipment before it ships. Include the invoice, packing photos, and carrier booking confirmation. If something goes wrong, you have everything in one place.

How does freight insurance differ from carrier liability?

Carrier liability is a legal obligation, not insurance. Carrier liability caps compensation at a contractual limit and requires the shipper to prove the carrier caused the loss. Freight insurance is a first-party contract that pays the cargo owner directly based on the insured value, minus any deductible.

The financial gap between the two is significant for ecommerce sellers:

- Weight-based caps: Carrier liability is often calculated at $0.50–$1.00 per pound. A 10-pound electronics shipment worth $500 may receive a maximum payout of $10.

- Burden of proof: To collect from a carrier, you must prove negligence. To collect from your insurer, you generally only need to prove the loss occurred.

- Legal frameworks: Domestic US trucking liability is governed by the Carmack Amendment, which sets strict notice requirements and limits recoverable damages. International shipments fall under conventions like the Montreal Convention for air freight or the Hague-Visby Rules for ocean cargo.

- High-value and lightweight goods: Electronics, jewelry, and apparel are the categories most severely underprotected by carrier liability alone.

| Protection Type | Basis for Payout | Typical Limit |

|---|---|---|

| Carrier liability | Weight per pound | $0.50–$1.00 per pound |

| Freight insurance | Declared cargo value | Up to full invoice value |

Sellers shipping goods where invoice value far exceeds the weight-based carrier cap need freight insurance. There is no workaround through carrier liability alone. Understanding freight class basics also matters here, because freight class affects both shipping costs and the baseline assumptions carriers use when calculating liability.

What practical tips help sellers choose and manage freight insurance?

Choosing the right policy starts with knowing your shipment profile. Sellers with frequent, high-volume shipments benefit most from open cargo policies. Open cargo policies provide automatic coverage for every shipment under a single annual contract, eliminating the need to bind coverage shipment by shipment. Per-shipment policies work for occasional or one-off freight needs.

Practical steps for managing freight insurance well:

- Verify exclusions before purchase. Read the full exclusions list, not just the coverage summary. Pay attention to packaging requirements, commodity restrictions, and vehicle security clauses.

- Match coverage to cargo value. Do not insure a $200 shipment the same way you insure a $20,000 one. Adjust declared value and deductibles to reflect actual risk.

- Document packaging to insurer standards. Some insurers publish specific packaging guidelines by commodity. Following them is not optional if you want claims paid.

- Compare coverage types by route risk. High-theft corridors, international routes, and temperature-sensitive lanes each carry different risk profiles. Named perils coverage may leave gaps on riskier routes.

- Choose insurers with transparent claims processes. Ask how long claims take, what documentation is required, and whether the insurer has a dedicated cargo claims team.

- Maintain a claims history log. Tracking your claims over time helps you negotiate better rates and identify patterns in loss events.

Freight insurance cost typically runs between 0.3% and 1% of the insured cargo value per shipment. That means a $10,000 shipment costs $30–$100 to insure. Measured against the cost of absorbing a total loss, the math is straightforward.

Pro Tip: If you ship internationally, ask your insurer whether your policy covers the full door-to-door journey, including inland transit at the destination country. Many policies only cover the ocean or air leg.

Key Takeaways

Freight insurance provides first-party cargo protection that carrier liability cannot replicate, and sellers who understand coverage types, exclusions, and claims requirements recover losses faster and more completely.

| Point | Details |

|---|---|

| All-risk is not all-inclusive | Exclusions like packaging failures and inherent vice are the leading causes of denied claims. |

| Carrier liability is insufficient alone | Weight-based caps of $0.50–$1.00 per pound severely underinsure high-value or lightweight goods. |

| Documentation drives claim outcomes | Photos, invoices, and delivery exceptions must be collected at the time of loss, not after. |

| Open cargo policies suit frequent shippers | Annual policies cover every shipment automatically, reducing per-shipment friction and cost. |

| Claims have strict deadlines | Incident reporting must occur within 30 days, with evidence submitted within 7–30 days. |

Why “all-risk” is the most misunderstood term in freight coverage

Most sellers I talk to assume “all-risk” means exactly that. It does not. The term is a legal shorthand for “all risks of physical loss or damage except those specifically excluded.” That distinction matters enormously when a claim is denied because the packaging was deemed inadequate or because the driver left the truck unattended at a rest stop overnight.

The uncomfortable truth is that the most common claim denials have nothing to do with obscure policy language. They come from operational failures that sellers control: poor packaging, missing delivery exception notes, and late reporting. I have seen businesses absorb five-figure losses on shipments that were technically insured, because they did not photograph the packaging or note damage on the delivery receipt.

Treating freight insurance as a checkbox rather than an operational discipline is the real risk. The policy is only as good as the documentation behind it. Sellers who build claims-ready habits into their shipping workflow, before anything goes wrong, are the ones who actually collect when it counts. Pairing solid insurance with a long-distance shipping strategy that accounts for route risk and carrier selection closes most of the remaining exposure.

— Maayan

How Or-ner supports smarter freight risk management

Managing freight insurance is easier when your logistics platform gives you full visibility into every shipment from booking to delivery. Or-ner integrates freight booking, real-time tracking, and exception management into one place, so sellers have the documentation trail they need before a claim ever arises.

Or-ner’s global logistics platform supports ecommerce sellers across ocean, air, and land transport, with tools that flag delivery exceptions, maintain shipment records, and connect sellers to reliable courier services worldwide. For sellers managing cross-border freight, Or-ner’s end-to-end visibility means you always have the evidence insurers ask for. Explore how Or-ner’s freight booking process can reduce your exposure and keep your shipments protected from origin to destination.

FAQ

What is freight insurance in simple terms?

Freight insurance, also called cargo insurance, is a policy that pays the cargo owner for physical loss or damage to goods during transit. It covers the declared value of the shipment, not just what the carrier is legally required to pay.

Does carrier liability replace freight insurance?

Carrier liability does not replace freight insurance. Carrier liability caps payouts at weight-based limits, often $0.50–$1.00 per pound, which covers only a fraction of most shipments’ actual value.

What causes most freight insurance claims to be denied?

Most claim denials result from inadequate packaging, violated policy conditions such as unattended vehicle clauses, and late or incomplete reporting. These are operational failures, not policy gaps.

How much does freight insurance cost per shipment?

Freight insurance typically costs between 0.3% and 1% of the insured cargo value per shipment, adjusted for commodity type and route risk.

What is an open cargo policy and who needs one?

An open cargo policy provides automatic coverage for all shipments under a single annual contract. It is best suited for ecommerce sellers and businesses that ship frequently and want to avoid binding coverage for each individual shipment.